Kotak Mahindra Bank Limited, AMFI Registered Mutual Fund Distributor , ARN 1390

May - 2026

| ▮ |

Market Summary |

Global and Indian equity markets rallied sharply in April 2026 despite the ongoing geopolitical conflict and volatile crude oil prices. Expectations of a peace deal between the US and Iran, steady corporate earnings, and a risk-on sentiment aided the recovery in equity markets. MSCI World and MSCI EM indices advanced 9.6% and 14.7% (in USD terms), respectively, while MSCI India gained 9.2%.

In April 2026, Nifty delivered +7.2% returns, while mid-cap and small-cap indices delivered +12.84% and +16.54% (in INR) respectively. As a result, domestic market has recovered in April 2026.

Foreign Portfolio Investors (FPI) recorded net outflows of INR 70,135.46 Cr in April 2026. However, DII inflows remained positive with INR 51,063.87 Cr. Equity funds logged positive inflows for the 62nd consecutive month, amounting to INR 38,440 Cr.

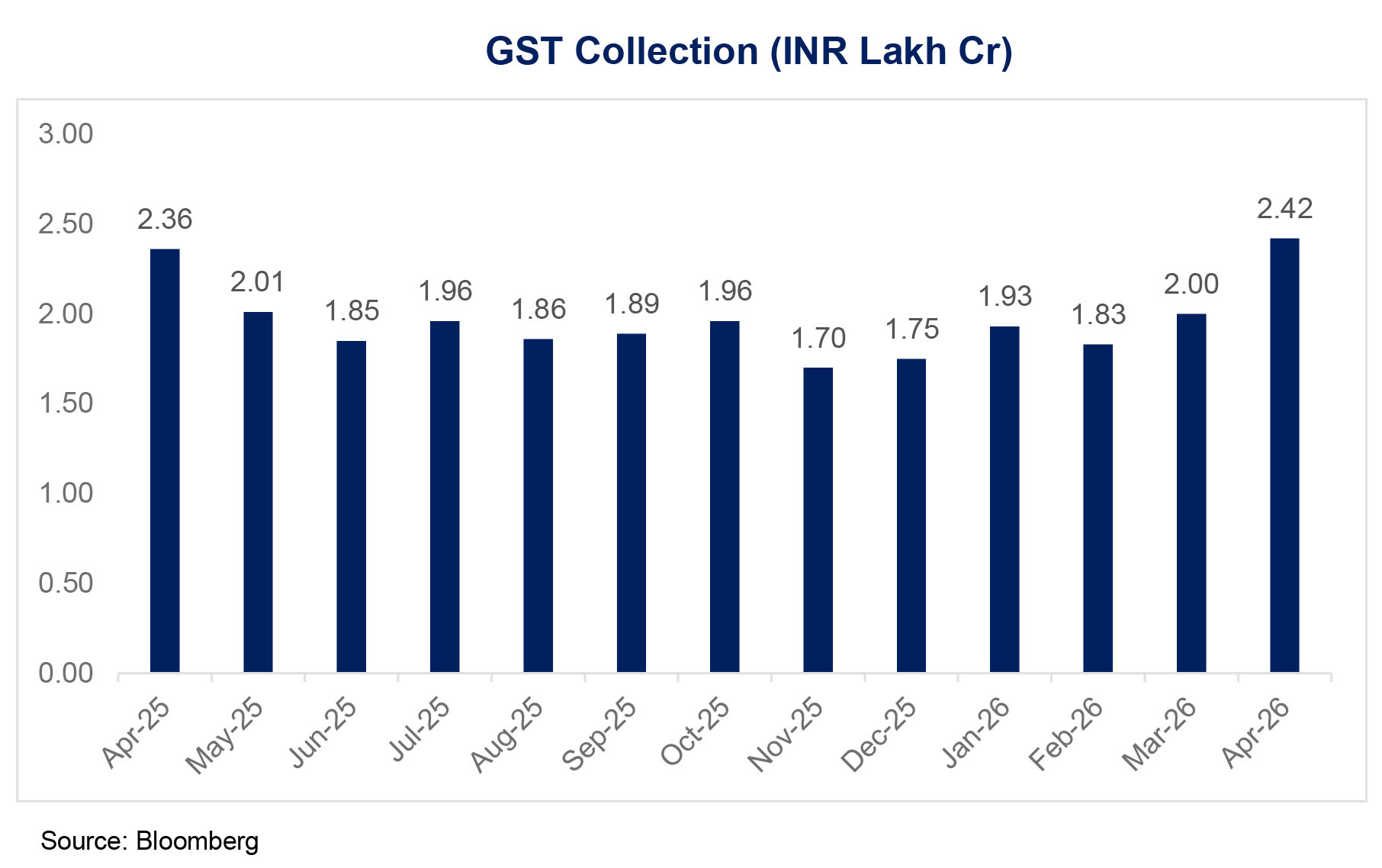

Remains resilient, as Manufacturing and Services PMI improving in April 2026 versus March 2026. Vehicle registrations were strong, power demand rebounded, and GST collections hit an all-time high of INR 2.42 lakh Cr, despite ongoing conflict and supply chain disruptions.

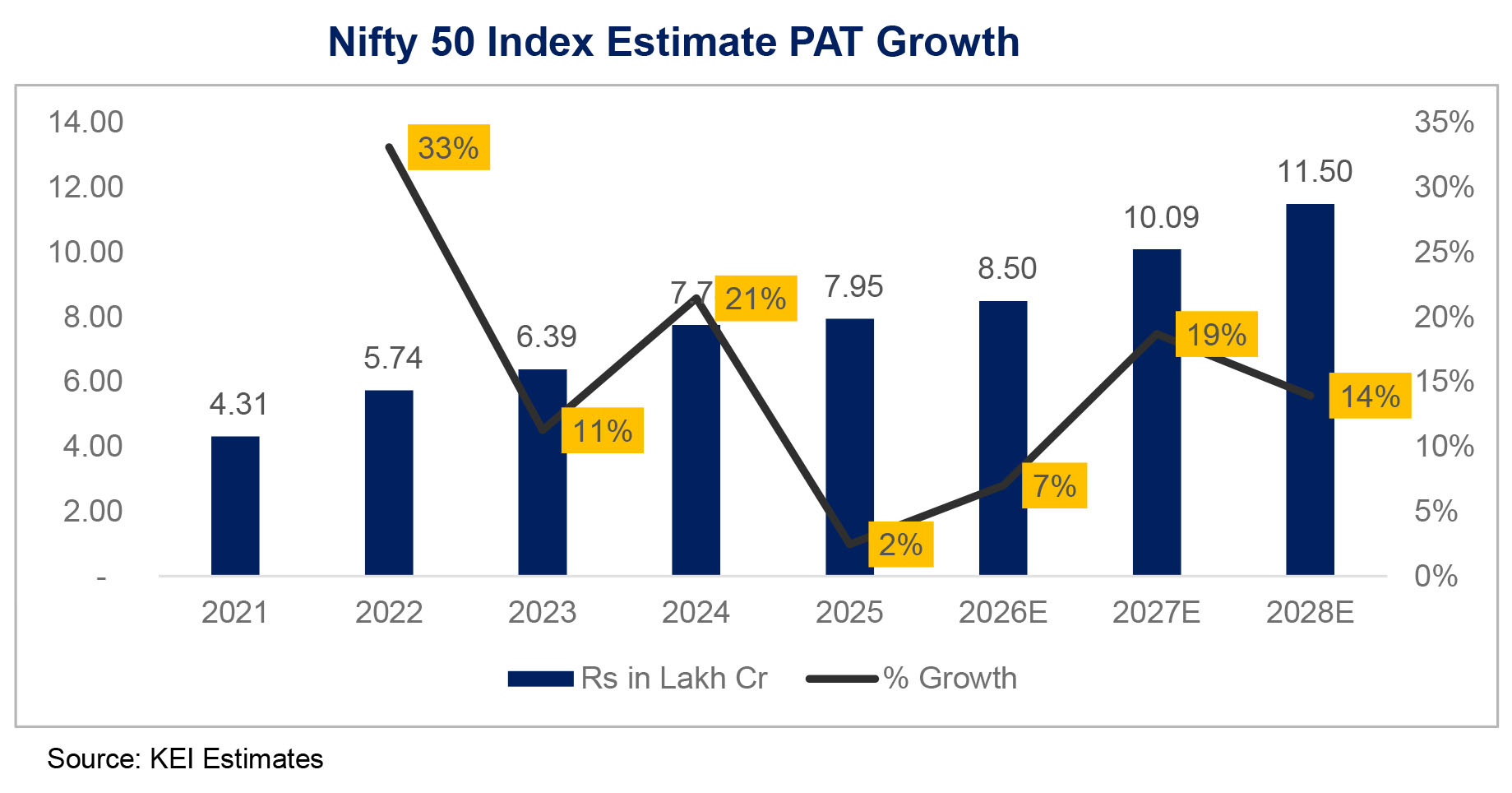

As per Kotak Institutional Equities Research, Nifty 50 earnings are expected to grow by 19.1% in FY27. The Nifty-50 Index is trading at 19.4x FY2027E and 16.9x FY2028E.

Source: Bloomberg, AMFI

| ▮ |

Outlook - Mutual Fund Investments |

• Delays in resolving the West Asia crisis pose a key risk to India's macros and earnings. Industrial output may weaken if energy prices stay elevated and supply pressure mounts.

• India Equities are trading at reasonable valuations after time and price correction over the past ~19 months. Valuations are meaningfully lower from 2024 highs and near historical averages, despite the April moderations

• The Federal Reserve left its benchmark interest rate unchanged at its April 2026 policy meet. Markets are now expecting Fed to hold rates until June 2027.

• We expect the RBI's surplus transfer to be in the range of ₹2.7-3.6 trillion, while maintaining the Centre's fiscal deficit estimate at 4.4%, though a slippage of 20-30 bps remains a key risk.

• We maintain a constructive stance on Indian equities market. Clients may consider up to 5% overweight on equities, as compared to their strategic equity allocation. Domestic-to-international equity mix: of 75%:25% may be considered.

• Clients may choose a 65%:35% allocation between large caps and mid & small caps, with value emerging in select parts of the mid- and small-cap space.

• We remain overweight on BFSI and positive on consumption, supported by a recovery in both rural and urban demand. Within consumption, we prefer discretionary over staples.

• Clients may maintain a 5% allocation to gold for diversification.

| ▮ |

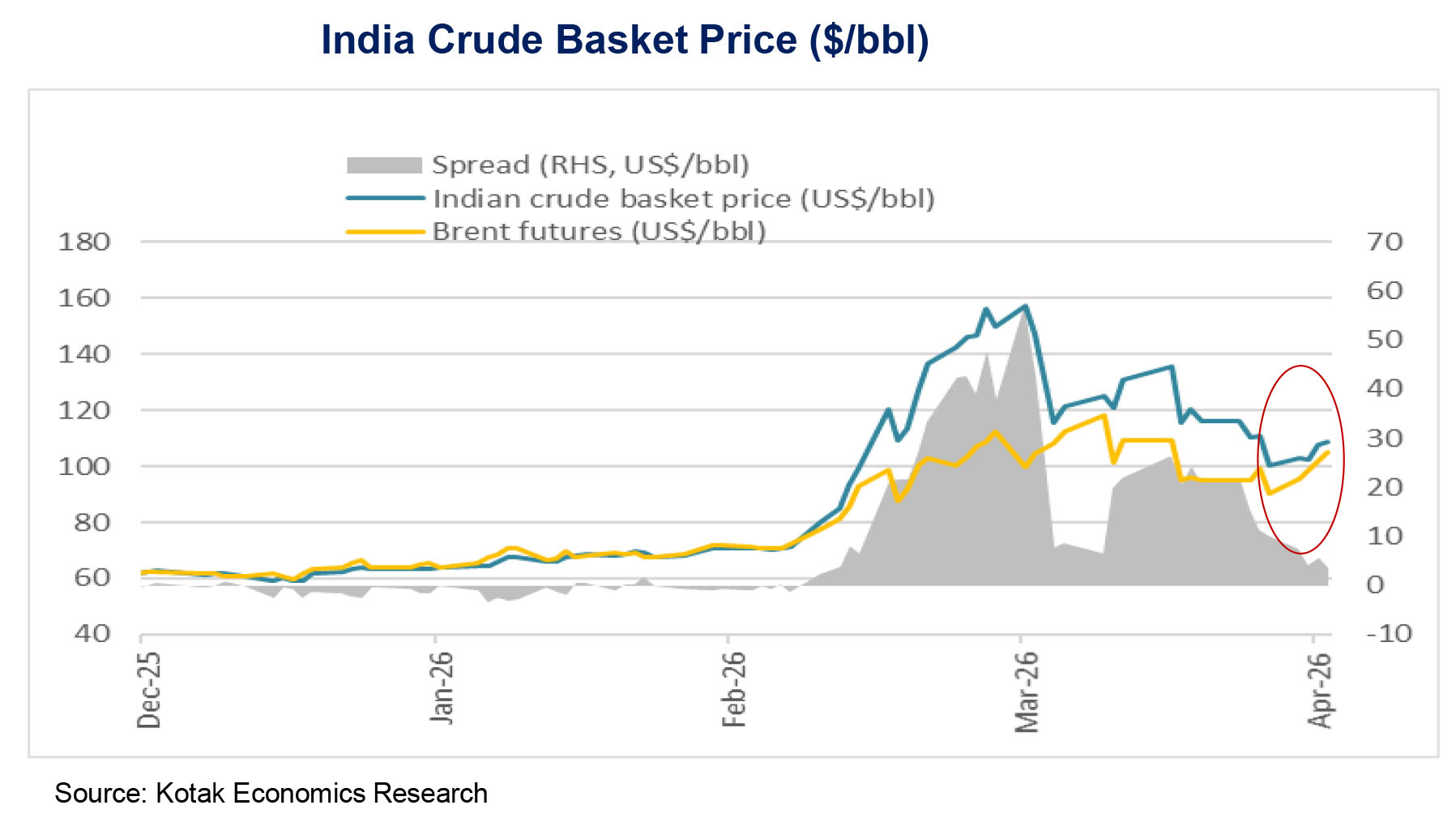

Crude Oil Supply & Price Movement |

• Indian Crude oil supply improved in April from Russia, Saudi Arabia, and UAE. Easing US sanction has also boosted supply.

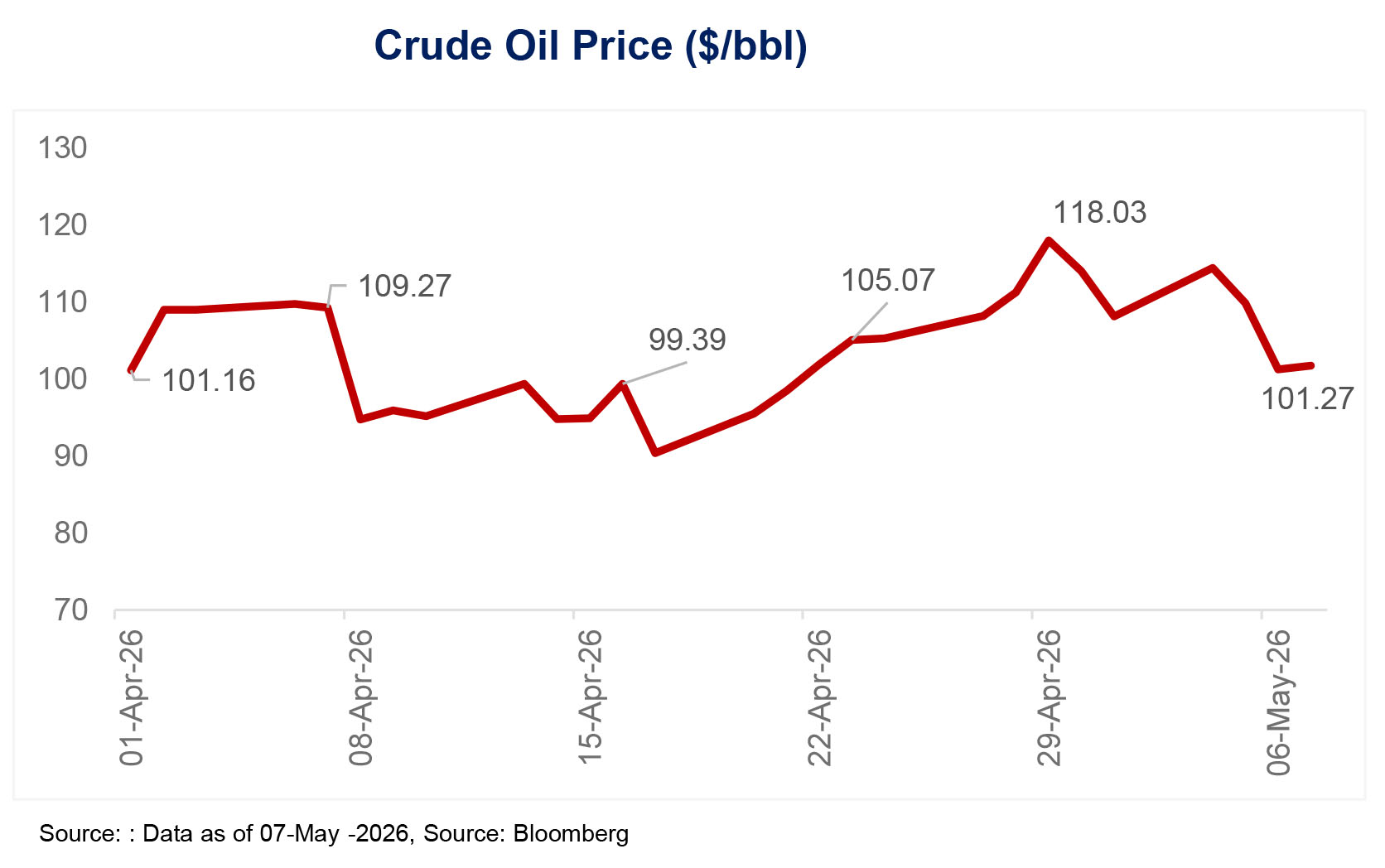

• Brent crude prices strengthened from ~USD 95/bbl in early April to ~USD 102/bbl in early May, driven by elevated geopolitical risk and supply concerns, before moderating on news of an MoU being signed between the US and Iran.

• Risk sentiment continues to remain favorable on hopes of a US-Iran peace deal. Reports indicate that both sides are edging closer to a one-page, 14-point MoU that could formally end the conflict and potentially reopen the Strait of Hormuz.

• RBI has been conscious of the negative fallout over the West Asia crisis, which is reflected in the ECLGC (Emergency Credit Line Guarantee Scheme) 5.0 for the MSME sector. RBI appears committed to providing sufficient liquidity.

| ▮ |

India Nominal GDP Growth Remains Strong |

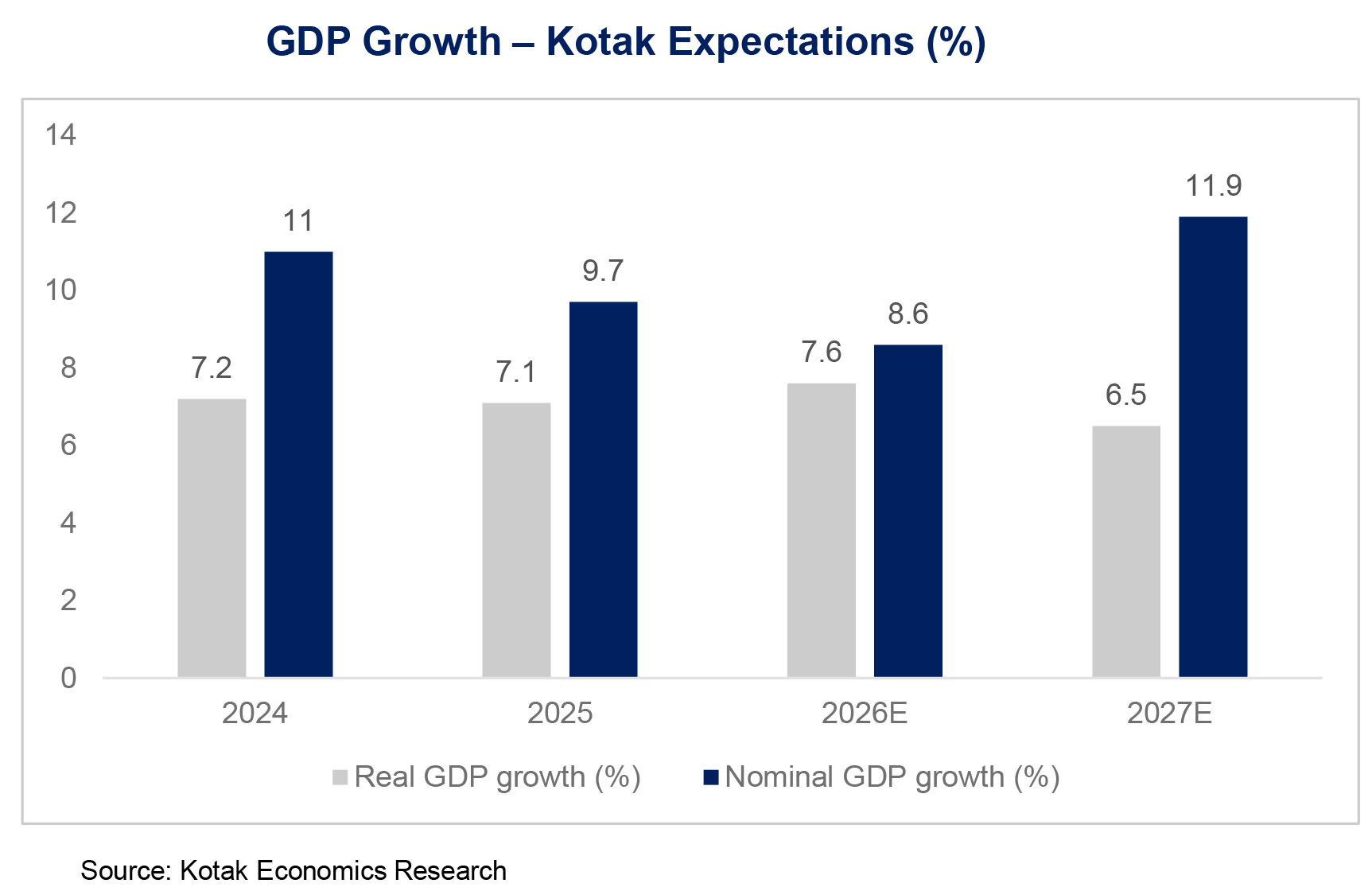

• In FY27, real GDP growth is expected at 6.5%, making India one of the fastest-growing economies globally. Nominal GDP is expected to grow at 11.9%, rising inflation, which could bode well for corporate profit growth.

• Domestic demand, Improving rural sentiment, and consumption-led growth, along with continued government capex, are expected to support growth. The broader market is expected to deliver better earnings growth.

• GST collections reached a record high of ₹2.43 lakh crore in April 2026, up 8.7% YoY from ₹2.23 lakh crore in April 2025, underscoring robust domestic economic strength.

| ▮ |

Corporate Profit Growth |

• India's earnings may hold up better than the broader economy in the event of a prolonged conflict (a few months), given the earnings composition of the market, particularly In the case of the Nifty-50 Index.

• We expect net profits of the Nifty-50 Index to grow by 19% in FY2027 and 14% in FY2028.

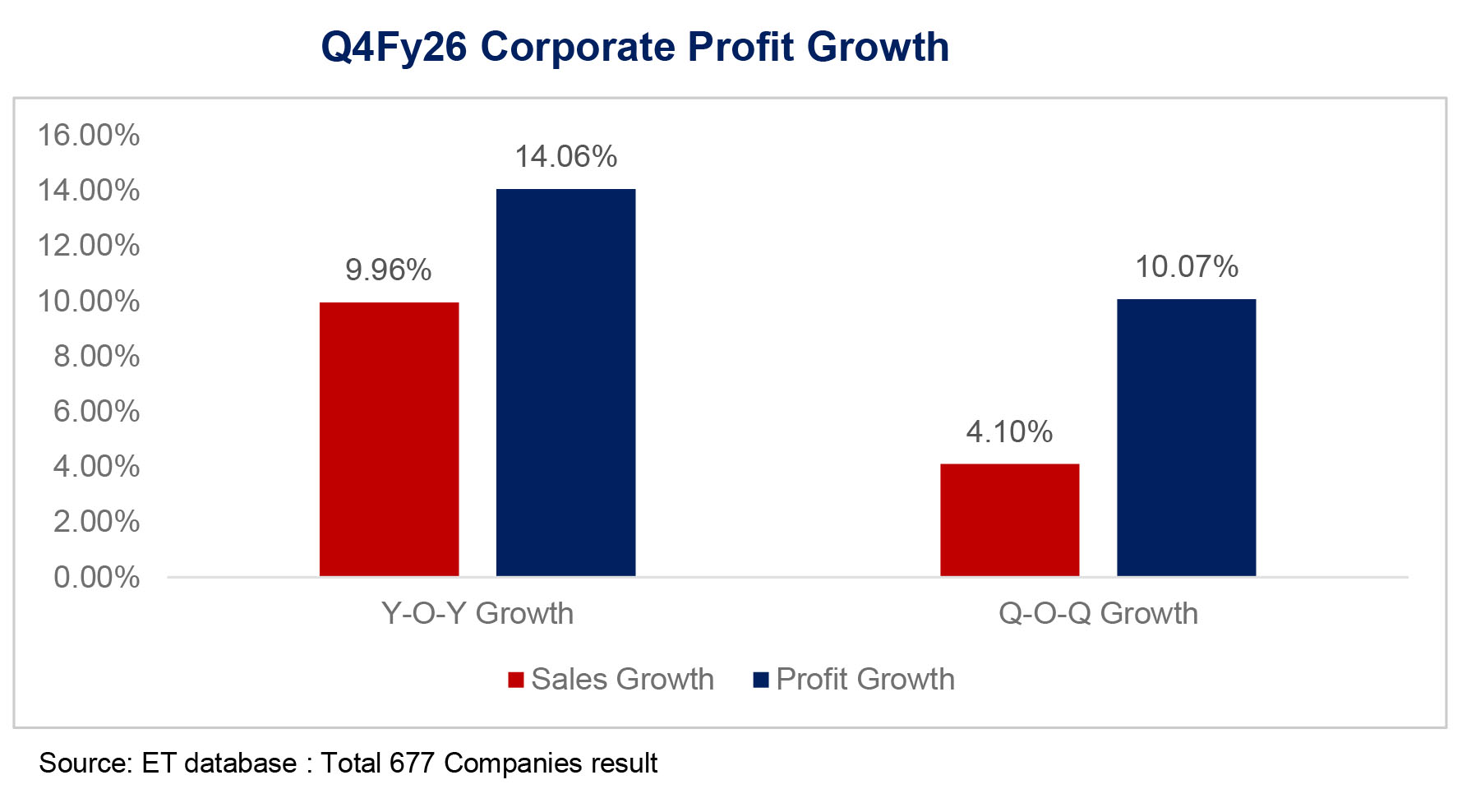

• Indian companies are reporting strong YoY profit growth in Q4FY26.

| ▮ |

Equity Valuations Ease |

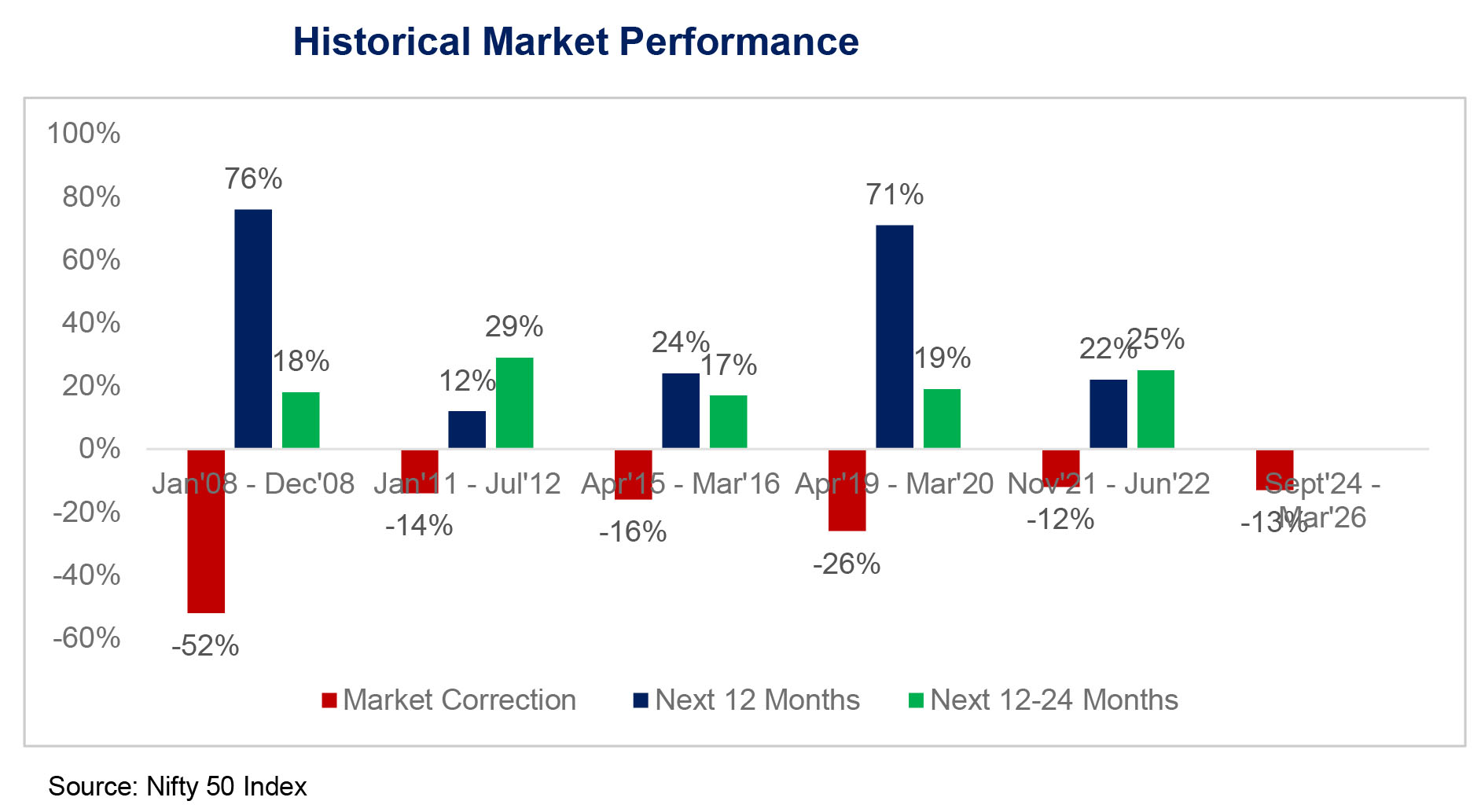

• In the past, sharp market falls were often followed by strong returns over the next 12 to 24 months. Markets corrected during the Global Financial Crisis (2008), the period of higher twin deficits in (2011-12), Banking NPA issues (2015-16), the COVID crisis (2020), and the Russia & Ukraine War (2021-22), and recovered sharply over the subsequent 12-24 months.

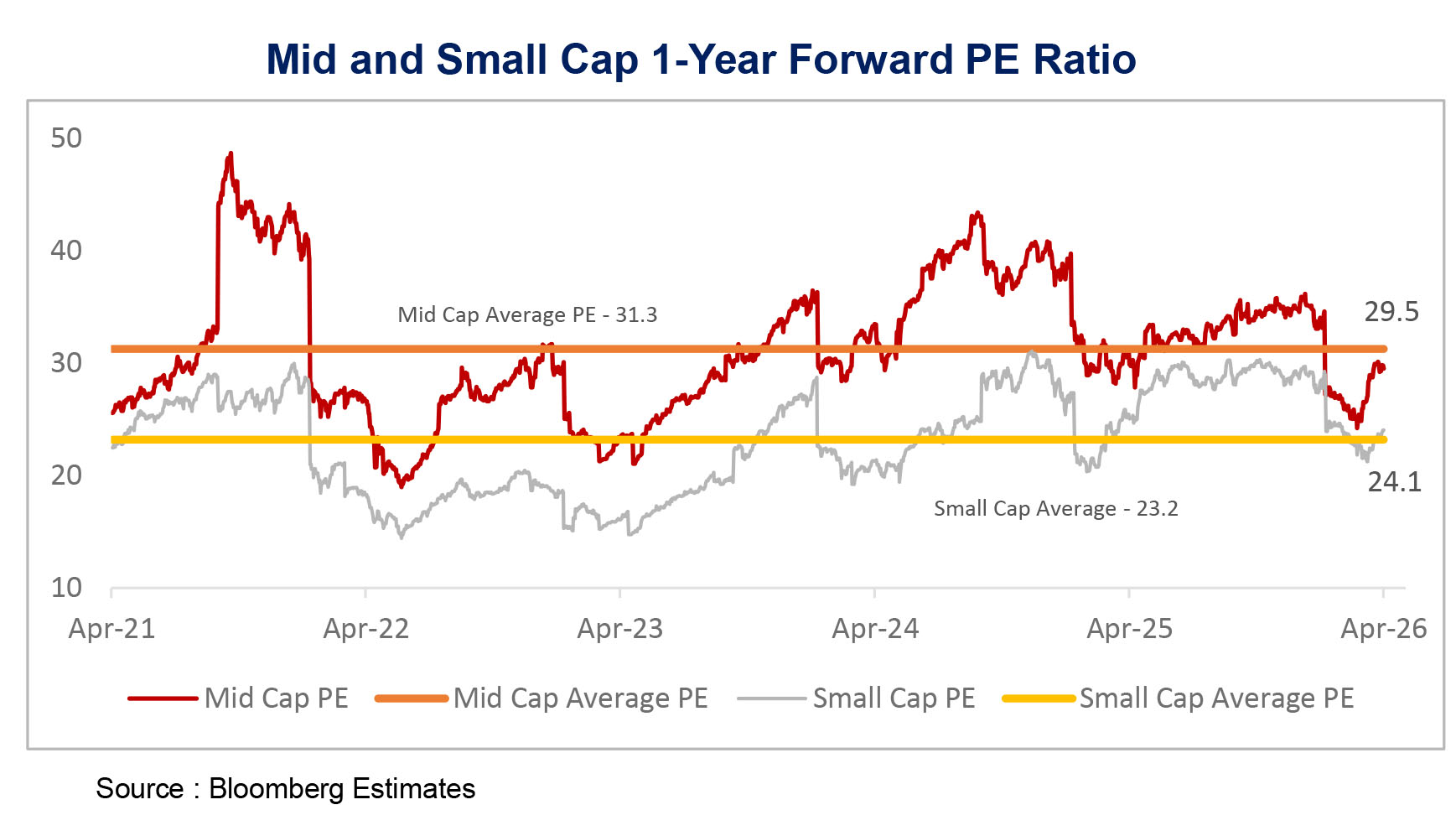

• Valuations of mid-cap and small-cap indices are near their five-year averages. After a period of correction, mid-and small-cap 1-year forward PEs are at their 5-year averages. Amid volatility, mid-and small-cap stocks have outperformed large cap in the current calendar year.

• Market corrections often reduce valuations and create better entry points for long-term wealth creation.

| ▮ |

Investment Summary for Mutual Fund Diversification |

| ▮ |

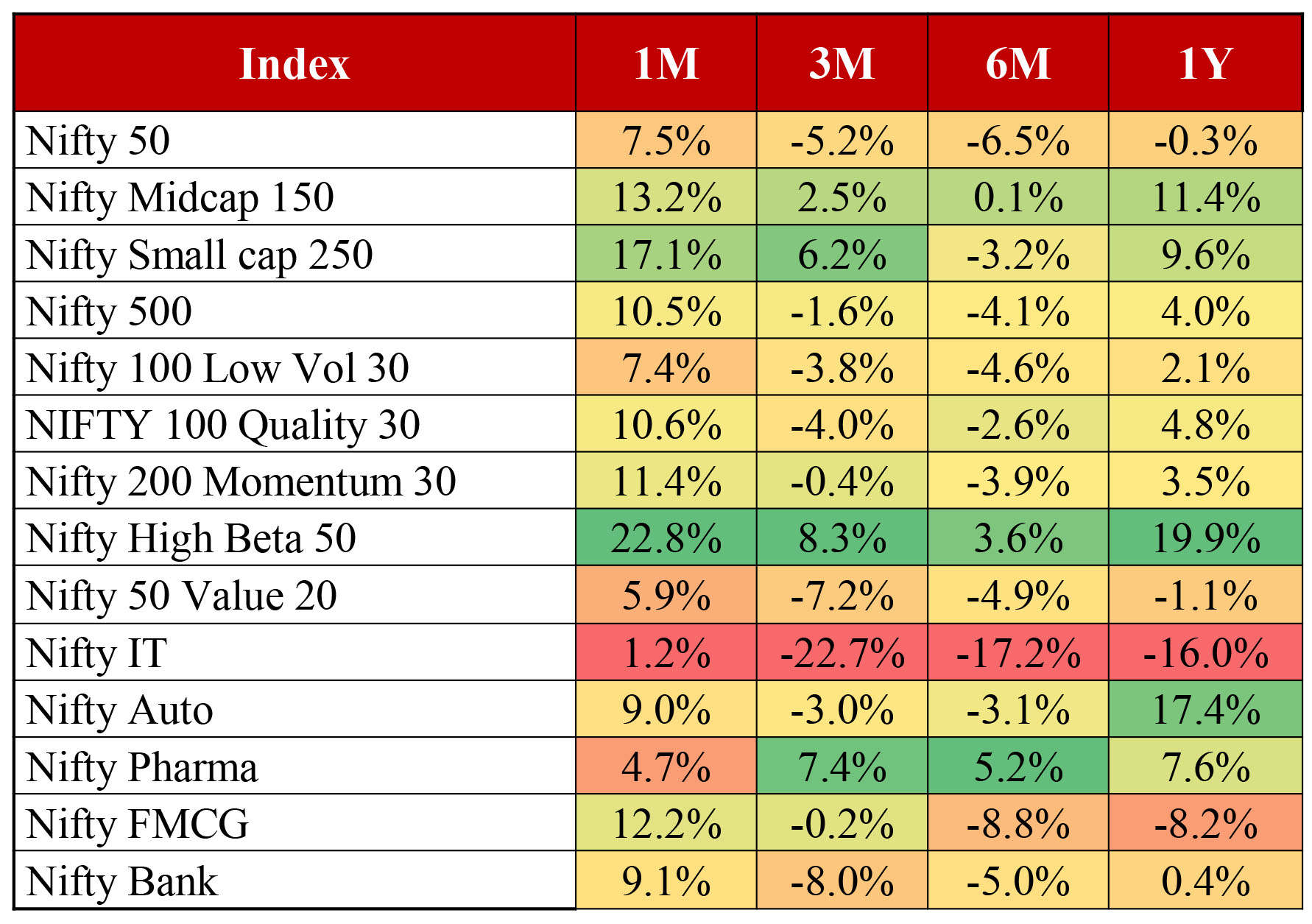

Domestic Market Performance |

Benchmark, Factor Indices & Sectoral Performance

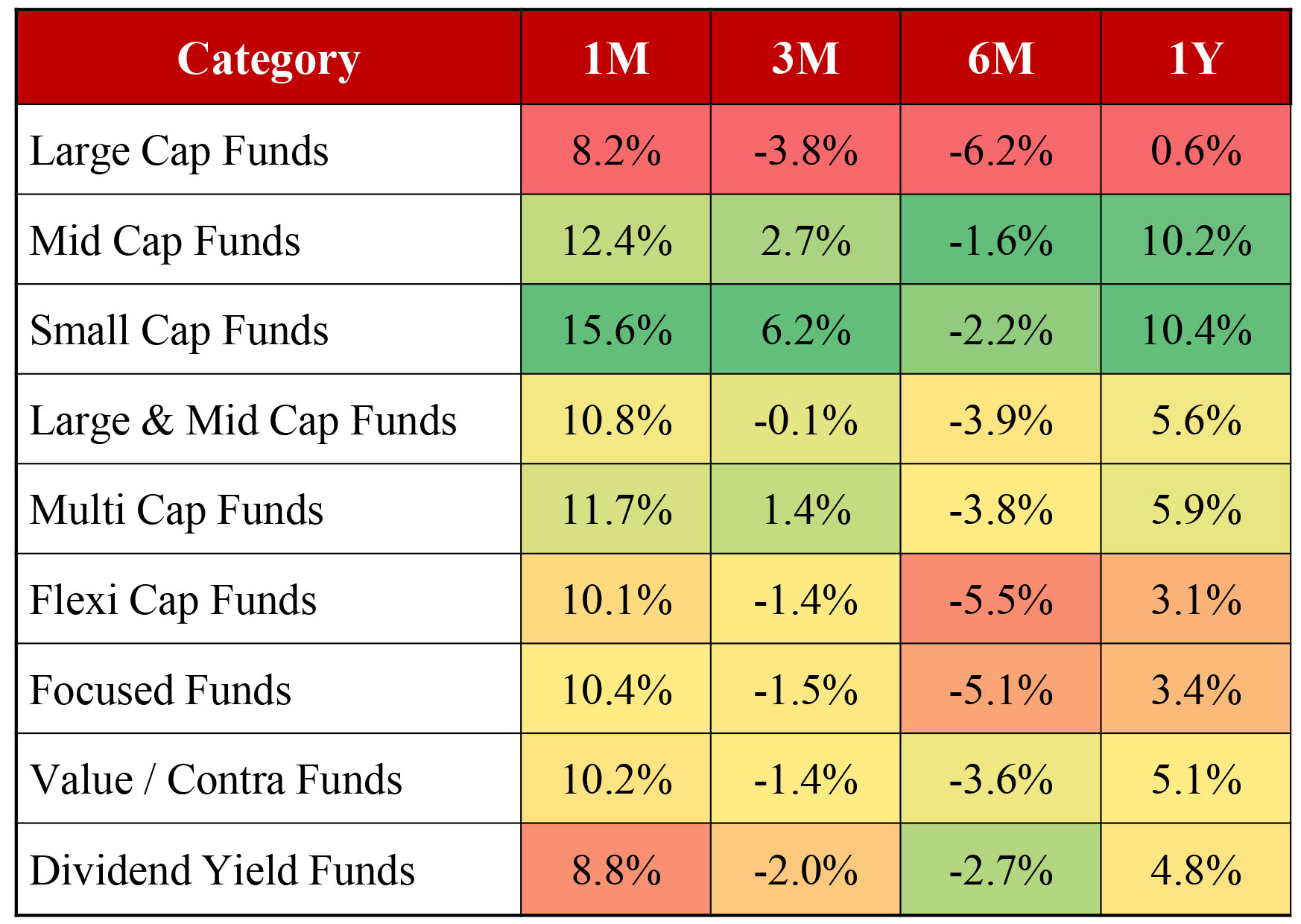

Equity MF Category wise Performance

Data as on 30th April 2026, Source: Bloomberg, ICRA

| ▮ | Disclaimer |

In the preparation of the material contained in this document, Kotak Mahindra Bank Ltd has used information that is publicly available, including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the Kotak Mahindra Bank Ltd and/or its affiliates and which may have been made available to Kotak Mahindra Bank Ltd and/or its affiliates. Information gathered & material used in this document are believed to be from reliable sources. Kotak Mahindra Bank Ltd however does not warrant the accuracy, reasonableness and/or completeness of any information. For data reference to any third party in this material no such party will assume any liability for the same. Kotak Mahindra Bank Ltd and/or any affiliate of Kotak Mahindra Bank Ltd does not in any way through this material solicit any offer for the purchase, sale or any financial transaction/commodities/products of any financial instrument dealt in this material. All recipients of this material should before dealing or transacting in any of the products referred to in this material make their own investigation, seek appropriate professional advice.

We have included statements/opinions/recommendations in this document which contain words or phrases such as "will", "expect" "should" and similar expressions or variations of such expressions, that are "forward-looking statements". Actual results may differ materially from those suggested by the forward-looking statements due to risks or uncertainties associated with our expectations with respect to, but not limited to, exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and/or investments, the monetary and interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic and foreign laws, regulations and taxes and changes in competition in the industry. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual future gains or losses could materially differ from those that have been estimated.

Kotak Mahindra Bank Ltd(including its affiliates) and any of its officers directors, personnel and employees, shall not liable for any loss, damage of any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any manner. The recipient alone shall be fully responsible/are liable for any decision taken on the basis of this material. The investments discussed in this material may not be suitable for all investors. Any person subscribing to or investing in any product/financial instruments should do so on the basis of and after verifying the terms attached to such product/financial instrument. Financial products and instruments, are subject to market risks and yields may fluctuate depending on various factors affecting capital/debt markets. Please note that past performance of the financial products and instruments does not necessarily indicate the future prospects and performance thereof. Such past performance may or may not be sustained in future. Kotak Mahindra Bank Ltd(including its affiliates) or its officers, directors, personnel and employees, including persons involved in the preparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities mentioned herein or(b) be engaged in any other transaction involving such securities and earn brokerage or other compensation in the financial instruments/products/commodities discussed herein or act as advisor or lender / borrower in respect of such securities/financial instruments/products/commodities or have other potential conflict of interest with respect to any recommendation and related information and opinions. The said persons may have acted upon and/or in a manner contradictory with the information contained here. No part of this material may be duplicated in whole or in part in any form and or redistributed without the prior written consent of Kotak Mahindra Bank Ltd. This material is strictly confidential to the recipient and should not be reproduced or disseminated to anyone else. Non-resident clients are advised to observe the limitations with regards to dealing in securities under the provisions of the Reserve Bank of India Act, 1934 (2 of 1934) for Non-Resident clients since the same have not been considered while arriving at the recommendations/advice made in this presentation.

Mutual Fund investments are subject to market risks. Please read the offer document carefully before investing.